Stablecoin Integration Signals Turning Point for Global Finance | Capital Nexus - By Shepley Capital

Welcome to the latest edition of Capital Nexus – Shepley Capital’s crypto newsletter.

Why Meta’s Stablecoin Integration Signals a Turning Point for Global Finance

In the second half of 2026, the digital financial system may cross a threshold that crypto advocates have anticipated for over a decade. Multiple massive institutions, led by Meta, are reportedly preparing to integrate stablecoin infrastructure directly into their platforms. This is not a speculative experiment or niche pilot. It represents a deliberate transition toward blockchain-based financial rails embedded into everyday digital life.

Meta alone controls Facebook, Instagram, and WhatsApp, giving it access to more than three billion users. Its current plan is to integrate third-party dollar-pegged stablecoins and launch a dedicated wallet to enable payments, creator payouts, and cross-border transfers across its ecosystem.

Unlike its failed Libra attempt, Meta is now choosing to partner with external stablecoin providers such as Stripe rather than issuing its own token. This approach reduces regulatory risk while still enabling the company to embed programmable digital dollars into its global payment flows.

At the same time, payment giant Stripe has significantly expanded its stablecoin activity and infrastructure, reflecting accelerating institutional commitment to tokenized money.

This convergence is not isolated. It is part of a broader shift where Big Tech, fintech, and financial institutions are positioning stablecoins as core financial infrastructure.

This is what it means for Aussie Retailers, and you… the spender.

For Australian retailers, stablecoin integration introduces something they have never had before. Instant, irreversible settlement without relying on traditional banking rails.

Today, when an Aussie business accepts a card payment, the money does not actually arrive immediately. It passes through multiple intermediaries. Payment processors. Acquiring banks. Settlement networks. Each taking fees. Each adding delay.

Stablecoins remove that friction entirely.

When platforms powered by companies like Meta Platforms and Stripe integrate stablecoin payments, an Australian retailer could:

– Receive funds instantly, not in 2 to 3 business days.

– Avoid significant merchant processing fees.

– Accept global payments as easily as domestic ones.

– Access revenue immediately for reinvestment or operations.

This directly improves cash flow. One of the most important survival metrics for small and medium-sized businesses.

It also removes one of the biggest barriers Australian retailers face. Geography.

For decades, Aussie businesses have been isolated by distance. Selling internationally meant:

– Foreign exchange fees

– International transfer delays

– Payment friction that reduced conversion rates

Stablecoins eliminate that disadvantage entirely, finally levelling the playing field for Aussie Retail & E-commerce together.

An Australian brand could sell to a customer in Brazil, Germany, or Singapore and receive USD stablecoins instantly. No bank approvals. No delays. No hidden conversion losses.

This opens global markets to Australian businesses at a scale previously only accessible to multinational corporations.

For you, the spender, the change will be subtle… in fact, you may not even realise you are using stablecoins.

Instead, you should begin to notice the following added perks:

– Refunds arriving instantly instead of days later.

– International purchases processing without foreign transaction fees.

– The ability to send money globally as easily as sending a message.

– Seamless payments directly inside apps you already use.

Money becomes faster. More fluid. More responsive.

And for the first time ever, holding & transferring digital dollars may not require a bank at all. This substancial evolution in the digital financial system introduces real competition to the traditional banking system, forceing the entire financial system to become more efficient:

– Lower fees.

– Better services.

– Faster settlement.

Even the Reserve Bank of Australia has acknowledged that tokenised forms of money and digital settlement infrastructure will play a major role in the future financial system.

The most important reality is that Stablecoins do not just improve crypto…

They improve commerce. They improve business. They improve the daily financial experience of ordinary people.

For Australian retailers, it removes geographic limitations.

For Australian consumers, it removes financial friction.

And for the global economy, it marks the beginning of money moving at the speed of the internet itself.

The AI Age Is Not Coming. It's Here.

We are no longer speculating about the AI era. We are living through its ignition phase where artificial intelligence is beginning to replace analysis, execution, research, coordination, and increasingly, independent decision making. The recent OpenClaw push toward autonomous AI agents operating 24 hours a day signals something far more significant than incremental progress. It signals completeness. AI is moving from tool to operator.

We are entering the AI Age of civilisation. And every civilisation shift is defined by infrastructure.

– The Industrial Age needed oil and steel.

– The Internet Age needed fiber and servers.

– The AI Age needs power and speed.

The Power Is Being Built.

Think about your own computer: to open a document, run a search, or load a game, thousands of micro processes execute simultaneously. Every click triggers layered instructions.

Now scale that to hundreds of millions of AI agents operating around the clock. Agents trading, negotiating contracts, managing supply chains, executing micro payments, coordinating logistics, and running entire businesses. That scale demands extraordinary computational energy. Companies like Nvidia & AMG are building that foundation, supplying the chips that power modern data centers and large scale AI models. Compute is scaling aggressively.

But compute alone is not enough. AI does not just think. It transacts. Every autonomous agent interacting with the real economy must send payments, validate data, record ownership, update contracts, and confirm state changes. That means transactions at machine speed. And this is where the structural bottleneck emerges.

Current blockchain infrastructure was not designed for machine scale commerce. Bitcoin processes roughly 7 transactions per second. It was engineered for security and decentralisation, not high frequency execution. Ethereum handles approximately 15 to 30 transactions per second on its base layer. Layer two solutions improve throughput, but base layer limitations remain significant. Ripple is often cited for speed and can process around 1,300 transactions per second. That is materially faster, yet still negligible relative to what a fully autonomous AI economy would require.

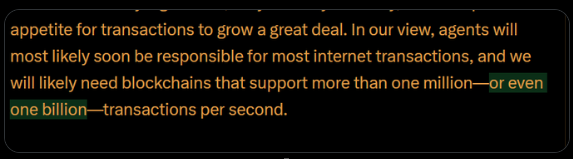

The real question is not whether these numbers are impressive relative to legacy systems. The real question is what is enough. If 100 million AI agents each execute only 10 transactions per minute, that equates to 1 billion transactions per minute, or over 16 million transactions per second… and that’s only a conservative estimate in a world where agents negotiate in milliseconds.

Leadership at Stripe has openly discussed how AI agents will require financial rails capable of supporting millions of transactions per second, potentially scaling toward the billion TPS range over time. Machine economies operate at machine velocity. Human speed is irrelevant.

Very few blockchains even claim throughput above 100,000 transactions per second, and even fewer approach 300,000 TPS in controlled environments.

And almost none architecturally target the million to billion TPS threshold required for full AI-scale adoption.

This is where emerging high-throughput architectures enter the conversation.

One of the few networks explicitly designed around extreme scalability is Keeta Network, which positions itself around ultra high throughput architecture, targeting hundreds of thousands of transactions per second with long term scalability toward significantly higher ranges. Whether any network can sustainably deliver those figures under real world decentralisation constraints remains to be validated. However, the direction of travel is undeniable.

Whether any network can truly sustain those numbers under real-world decentralization constraints remains to be proven. But the direction is clear.

The AI Age forces a throughput revolution. Compute without transaction rails is intelligence without action. If autonomous agents cannot settle value, execute agreements, or coordinate state changes instantly, the system collapses under friction. Blockchain was originally designed to serve human finance. It may ultimately be required to serve machine finance. Machines do not tolerate congestion, latency, or settlement delays.

History shows that infrastructure always trails innovation at first. Early internet bandwidth constrained digital media. Streaming services were once crippled by buffering. Cloud computing faced cost barriers before scale efficiencies emerged. AI will face a similar bottleneck in transaction throughput. Capital will inevitably flow toward whatever infrastructure can remove that constraint.

The defining question of the next decade is not whether AI transforms civilisation…

It is which digital transaction layer can sustain civilisation at machine scale.

PS: We’re going to start posting these individual long-form stories in our new ‘Shepley Journal’ catalogue on our website. If you want a second read or wish to show a friend what you read, you can find the link to our full catalogue on our ‘FREE RESOURCES’ page.

The Future of Stablecoins: 2026 Trends & Global Regulations

Stablecoins are the connective tissue of the digital financial system, acting as a stable bridge between the volatile world of cryptocurrencies and the traditional world of government-issued “fiat” currency. In 2026, we have moved past the era where stablecoins were merely a tool for traders to “park” their funds between deals. Today, they have evolved into a sophisticated layer of global financial infrastructure, essentially becoming the “Internet’s Dollar.”

See you next volume.

~ Chris Shepley

Founder of Shepley Capital

WRITTEN & REVIEWED BY Chris Shepley

UPDATED: MARCH 2026